Financial Planning in Singapore – 3 Things You Must Know Before Investing

Contributed by: Bryan Zeng

CFA, General Manager, FA Advisory Sdn Bhd

(The contributor can be contacted at bryanzeng@fa.my).

Regardless of whether you are in Singapore or anywhere else in the world, financial planning, especially saving and investing, is crucial for you to beat inflation or to achieve your financial goal, such as to have a comfortable retirement. You may have heard of people who lost their fortune during the 1997 Asian Financial Crisis or the 2007 Global Financial Crisis. However, when done right, investing can make an average person a millionaire.

Investing can be a risky endeavour, but help is at hand from financial advisory professionals in Singapore. Nevertheless, whether you wish to invest on your own or with the guidance of a financial adviser, do take some time to understand 3 “golden rules” everyone should know and practise in their investment journey:

-

Preserve your capital

“Rule No. 1: Never Lose Money. Rule No. 2: Never Forget Rule No. 1.” – Warren Buffett

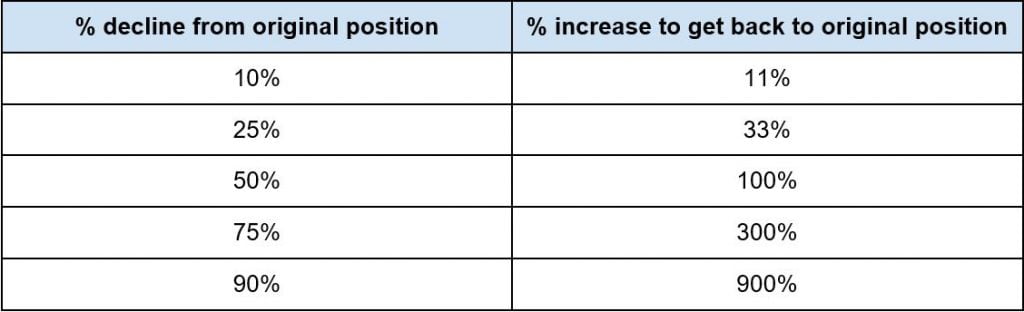

This timeless quote from Warren Buffett, one of the most successful investors of all time, reminds us of the importance of preserving our investment capital.The lesson here is not about avoiding the daily price volatility in the financial markets, but rather the need to guard against excessive losses, whether realised or unrealised. This is illustrated in the table below:

The left column of the table shows the percentage decline or losses from the original capital, while the right side shows the percentage of increase required to return to the original capital (breakeven) position after suffering the losses. As clearly illustrated in the table, a 10% loss would require a 11% gain to return to the original capital position, and a 25% loss would require a 33% gain to break even, so on and so forth.Putting this into an example, if you have invested $10,000 in your investment portfolio, and the portfolio suffered a 50% loss (which means the value has declined to $5,000), the portfolio would then need to generate a return of 100% – in other words, double its value from $5,000 to $10,000 – in order to break even. Even then, the portfolio will only be back to its original position and will have not made any gains yet!

The key point here is that you win by not losing. That is why when we manage investments for our clients in Singapore, we focus on the downside by not allowing excessive losses, and the upside will take care of itself.

-

Include Diversification as Part of Your Financial Planning Strategy

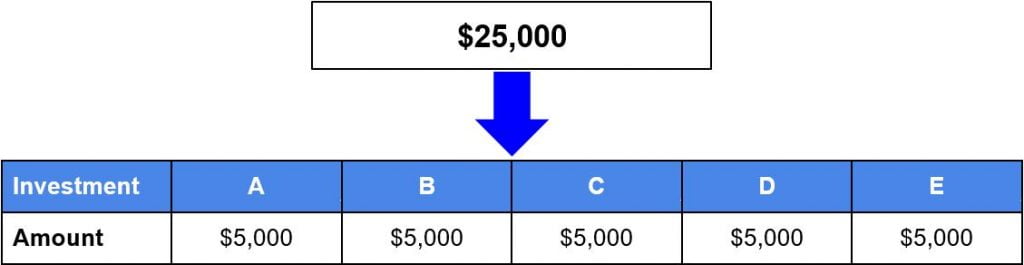

Suppose you have $25,000 to invest right now, but you are not sure of what investment to go into, therefore you take a very simplistic approach to invest $5,000 into 5 different investments in Singapore.

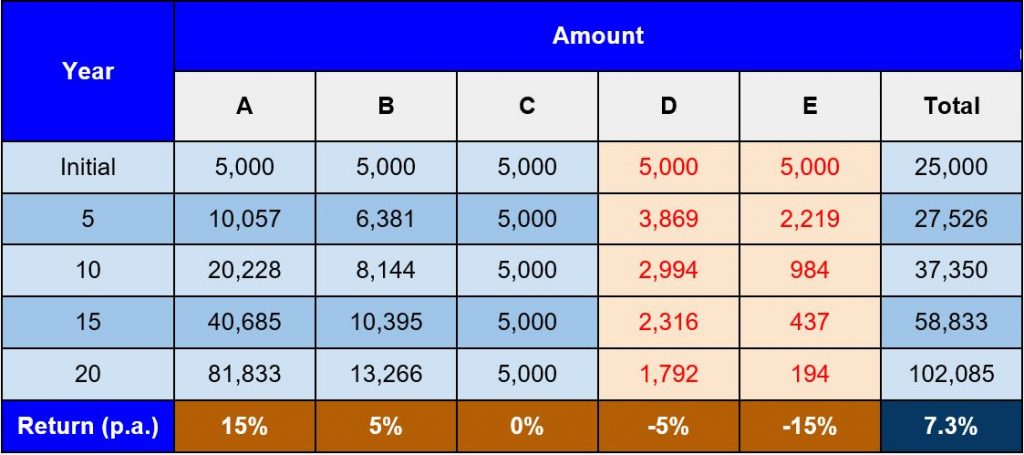

After 20 years, assume that the 5 investments in Singapore will yield the following results:

After 20 years, how much do you think your $25,000 have grown?

We may mistakenly think that our investment would have remained the same because the +15% and +5% returns seem to have been cancelled out by the -15% and -5% returns.

Thankfully, this is not the case and the actual results are shown in the table below.

Your $25,000 investment would have grown by more than 4 times to $102,085 after 20 years, giving an annual return of 7.3%!

This shows that, with diversification, even if one or two of your investments didn’t do well, you have a high probability of getting a positive return. You can find more about diversification here.

-

Keep your eye on the prize

“Always remember your ‘Why’”

Before we start investing or planning our financial future in Singapore, we must know why do we want to invest. We should have the end in mind. This could be a financial goal that we want to achieve, for example to accumulate a $5,000,000 retirement fund by age 60 or to raise $500,000 for a child’s tertiary education in 15 years. The goal has to be specific and measurable.

We must regularly review and monitor our investment plan. Make adjustments when necessary, to ensure that our investments are on track to realise our financial goals. If an investment is doing badly and the fundamentals have deteriorated, we may want to exit the investment and redeploy the capital to a better performing investment. If the overall plan seems to be falling short, then we may need to increase our savings to make up for the shortfall. On the other hand, if the investment is doing very well, we may want to lock in the gains early.

Financial planning and investing to achieve your financial objectives are not rocket science but doing them well would take time and effort. When investing, remember the three principles above and you would have established the right foundation for greater success. Alternatively, if you wish, you can engage a trusted financial advisory firm that provides investment planning as part of its financial consulting services.