Representatives of Financial Advisers see a Growing Demand for Their Services in Singapore

Contributed by Michelle Ee,

Wealth Management Director, Financial Alliance Pte Ltd

(The contributor can be contacted at michelleee@fa.sg)

Life insurance business in general is enjoying an uptrend in Singapore – but the three main life insurance distribution channels are facing mixed fortunes.

According to the Life Insurance Association of Singapore (“LIA”), the Singapore life insurance industry continues to grow briskly, with weighted premiums received by life insurance companies in the first half of 2017 to be 10% above those received in the first half of 2016. This has led me to take a broader look at how the three main life insurance distribution channels – namely the tied agents, banks and financial advisers – have fared in general in the last decade or so.

As there are tied agents who refer themselves as “financial advisers”, here’s a quick clarification for readers who might not be aware of the key difference between “tied agents” and “financial advisers” in Singapore (based on the way they are categorised in LIA’s reports). Tied agents are individuals who are restricted to only distributing products from the one-and-only life insurance company he/she is “tied” to. Representatives of financial advisers, on the other hand, are individuals who can source for a wider range of products from many life insurance companies to structure financial solutions.

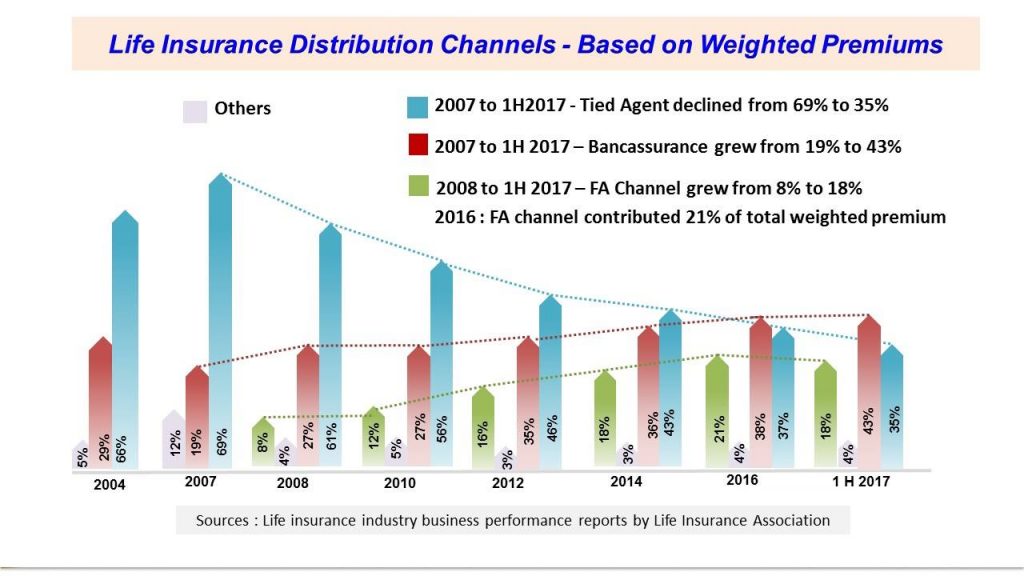

Since 2004, I have been collating the percentage of life insurance business distributed via tied agents, banks and financial advisers, and they are depicted in the graph below.

The steady upward growth trend for financial advisers and banks cannot be missed. During the same period, the tied agents channel experienced an unmistakable downward trend.

This change in trends suggests that consumers appear to be slowly, but inevitably, moving away from tied agents in favour of other channels, and financial advisers are well-placed to meet the requirements of consumers who seek holistic financial planning with suitable financial products from different sources.

As for the banks, they have capitalised on their captive databases of existing banking clients to give them a natural head start in capturing the market share from the moment they entered the life insurance market.

The population of tied agents is estimated to have remained at about 13,000 to 14,000 over the last 10 years. On the other hand, the number of financial adviser representatives has bloomed from a few hundred in 2002 to over 2,000 in about 10 years. Today, they number at about 3,000 to 3,500. This shows that in today’s market, individuals who turn to professionals when planning for their finances are more likely to engage a financial adviser representative. With such a big difference in manpower between the two channels, combined with their market share trends, it has been noted that productivity is higher among financial advisers’ representatives than among tied agents.

With the advent of robo-advisers, a growing population of savvy consumers and other exciting developments in the financial advisory industry, I do hope financial advisers raise their game further to meet these challenges and offer real value to the consumers and society in general.