8 Personal Financial Ratios to Check Before You Invest

Contributed by Kenny Loh

Senior Consultant, Financial Alliance Pte Ltd

(The contributor can be contacted at kennyloh@fapl.sg)

To learn more about him and read his articles, visit his blog

Like the physiotherapist who has to check the physical health of the professional soccer players before declaring them to be fully fit to play in a 90-minute competitive game, we as retail investors need to understand our own personal financial ratios so that we prioritise allocating our limited resources to the more pressing areas in our personal financial plans.

In short, don’t jump straight into investments if we are not sure of our financial “fitness level.” So how do we know what our fitness levels are?

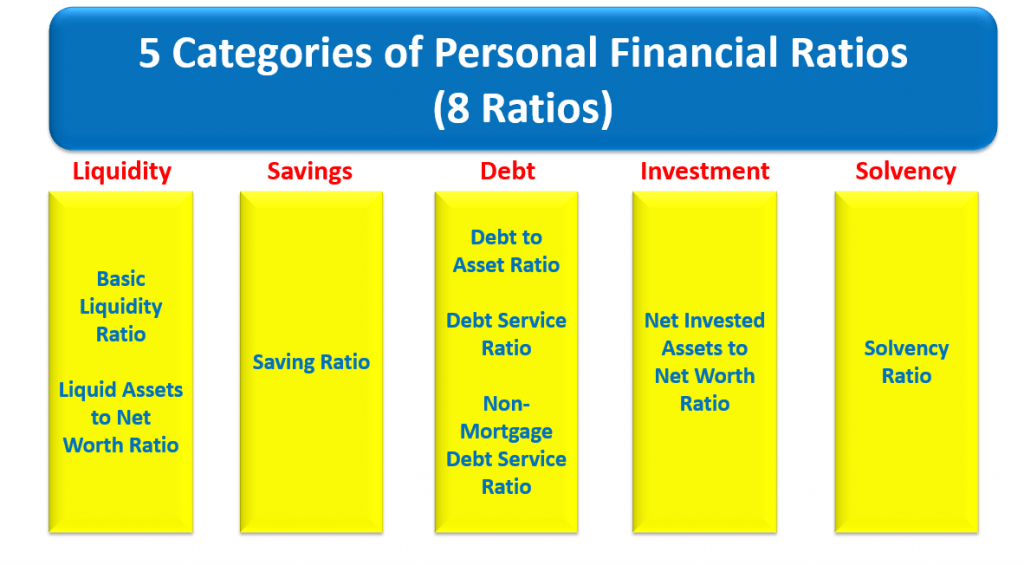

There are 8 basic personal financial ratios we need to check.

(1) Basic Liquidity Ratio (= Total Cash / Total Monthly Cash Outflow)

(1) Basic Liquidity Ratio (= Total Cash / Total Monthly Cash Outflow)

This ratio tells us whether we have enough cash reserves to service our monthly expenses. A good ballpark guideline for a typical person is 3 to 6 months, but unemployed PMETs (professionals, managers, executives and technicians) who are aged 40 and above may need up to 1 year because they may need a longer time to find a job. In other words, this can be treated as the number of months’ emergency fund available to deal with unforeseen circumstances.

(2) Liquid Assets to Net Worth Ratio (= Total Cash / Net Worth)

This ratio indicates the percentage of your net worth that is liquid. If you are a retiree and you think you may have “Asset Rich Cash Poor” symptoms, check whether your ratio is meeting at least 15% of the guideline.

(3) Savings Ratio (= Monthly Savings for Investment / Gross Monthly Income)

This ratio measures whether one sets aside part of the monthly income to invest regularly with discipline to meet their own financial goals. As a general rule of thumb, one should put aside at least 10% of one’s monthly gross income. In other words, “Pay Yourself” first!

(4) Debt to Asset Ratio (= Total Liabilities / Total Assets)

This is also known as personal Gearing Ratio. This ratio checks how much your assets are funded by debt. As a general rule of thumb, you should have no more than 50% of your assets leveraged through debt.

(5) Debt Service Ratio (= All Debt Repayment / Net Monthly Income)

This ratio measures how much you use your “take-home-pay” to service total debt obligations. If you don’t want to become a housing loan, credit card loan or any debt slave, start reducing your Debt Service Ratio to less than 35%, as per the general guideline.

(6) Non-Mortgage Debt Service Ratio (= Non-Mortgage Debt / Net Monthly Income)

This ratio measures how much you use your “take-home-pay” to service your credit card debt, personal loan and other non-mortgage related debt. The effective interest rates of all these debts are much higher than mortgage loan. If you are in financial distress and facing difficulties in clearing your debt, this is the area you should focus on immediately. As a general rule of thumb, you should have no more than 15% of your net income going into non-mortgage debt.

(7) Net Investment Assets to Net Worth Ratio (= Total Invested Assets / Net Worth)

This ratio measures how much your net worth is invested in assets, and whether you deploy the resources efficiently to income-generating asset classes. As a general guideline, you should have at least 50% of your assets invested in some form of capital (investment) assets.

(8) Solvency Ratio (= Net Worth / Total Assets)

This ratio measures your technical solvency in terms of whether you have sufficient assets to meet your liabilities. As a general rule of thumb, your Net Worth should be at least 50% of your Total Assets.

In summary, understanding our own personal financial ratios is extremely important when charting our financial journey to prioritise the allocation of our limited financial resources. Personal financial ratios also serve as measurements of our financial progress as we move along our life stages. Things get measured, and things get done and improved. Start determining your personal financial ratios now.