Bond 101: 5 Things You Need to Know – What is a Bond?

This is the first of a series of articles to help you gain a basic understanding of bonds as an asset class and its role in portfolio planning.

1. What is the Size of the Global Bond Market?

The global bond market is $105.9 trillion – which is larger than the global equity market capitalization of $95.0 trillion as of 2019 – according to the Securities Industry and Financial Markets Association (SIFMA)[1]. Given its size, this is an asset class we should not ignore.

2. What is a Bond?

A bond is a loan made to the bond issuer. Issuers like governments, corporations, and government agencies issue bonds when they need capital to finance their projects or operations. Just like a loan, a bond pays interest regularly and repays the principal at a stated time, known as maturity. Therefore, the bondholder is a creditor, not a shareholder.

3. Why is a Bond Attractive for Retirees, Pension Funds, and Insurance Companies?

A bond is generally relatively less risky than equity. In the event of liquidation, bondholders get repaid before shareholders as bonds rank higher than equity for distribution.

As a creditor, the bondholder has a higher probability of getting their capital investment back than the shareholder. Additionally, bond interest is paid typically half-yearly, providing a stable source of income that is attractive for retirees, pension funds, and insurance companies.

4. How is Bond Interest Determined by the Issuer?

A bond is typically issued with the par value, a maturity date, and the coupon rate. The par value – or the face value – of the bond is the amount borrowed by the issuer and the maturity date determines when the amount borrowed will be eventually repaid. The coupon rate is the interest rate to be paid periodically by the issuer.

The issuer has to consider the prevailing interest rate environment to ensure that the coupon is competitive and attractive to investors for comparable bonds. For example, a corporation that issues a 10-year bond of par value of $1,000 with an annual coupon of 5% will have to repay the $1,000 face value to each bondholder upon the bond’s maturity at the end of 10 years.

The duration taken for a bond to reach maturity typically determines the risk as well as the potential return an investor can expect. A $1 million bond repaid in 10 years is considered relatively less risky than the same bond repaid at the end of 30 years.

The reason for this is that 30 years give rise to a higher probability of negative factors affecting the issuer’s ability to repay bondholders than 10 years. In other words, the issuer in this example should pay a higher coupon on the 30-year bond to induce investors to undertake additional duration risk.

Not all bonds are the same. Some bonds may carry a higher risk that the issuer may “default” on the loan or fail to fully repay the loan.

Independent credit rating services such as Moody and S&P assess the default risk, or credit risk, of bond issuers and publish credit ratings regularly on the issuer. Investors who purchase bonds with lower credit ratings can potentially earn higher returns but they must at the same time bear the additional risk of default by the bond issuer.

5. What are the Types of Bond?

In general, government and corporate bonds are the two largest sectors of the bond market, but other types of bonds such as mortgage-backed securities and asset-backed securities are designed to meet the investment needs of specific sectors.

The government bond sector is a broad category that includes “sovereign” debt, which is issued by a central government and may also include agency and “quasi-government” bonds. While the USA, Japan, and Europe have historically been the biggest issuers in the government bond market, the Chinese government is the emerging leader after the USA and may overtake the USA[2].

The corporate bond sector is the second largest segment of the bond market. Corporations issue bonds to meet their funding needs. Corporate bonds can be classified into two broad categories: investment-grade and speculative-grade (also known as high-yield or “junk”) bonds.

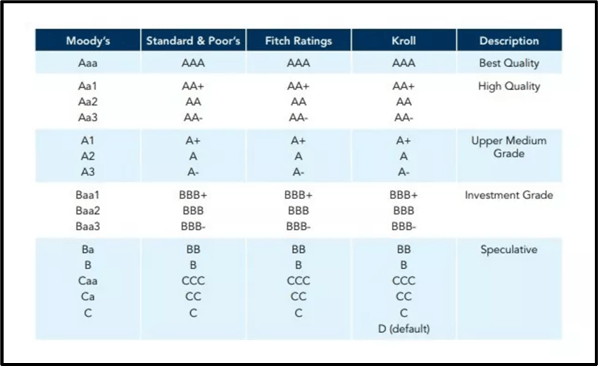

Speculative-grade bonds are issued by companies deemed to have lower credit quality and therefore higher default risk compared with investment-grade companies. The major credit rating agencies provide a wide range of ratings reflecting the fact that the fundamental and financial health of issuers can vary quite substantially. Please see the chart below.

Credit Rating by Top Rating Service Agencies

Speculative-grade bonds are more likely to be issued by start-up companies, companies in highly volatile sectors, or companies in weaker financial health.

Hence, a speculative-grade credit rating would require a higher coupon to compensate investors for the higher risk. Credit ratings are updated regularly by rating service agencies and can be downgraded or upgraded based on changes to the issuer’s fundamentals and financial health.

What’s Next?

In the next 2 articles – Bond 102 – we will explore bond pricing in the open market. In Bond 103, we will explore the role of bonds in portfolio planning in a rising interest rate environment.

References:

- 1. SIFMA 2020 Capital Market Fact Book. https://www.sifma.org/resources/research/fact-book/

- 2. China bonding with the World. https://www.ipe.com/home/briefing-china-bonding-with-the-world/10053023.article

- 3. Vanguard research team, “What is a bond? A way to get income and stability”

- 4. PIMCO research team, “Understanding investing – Bond”

- 5. iFast research team, “What is a bond?”